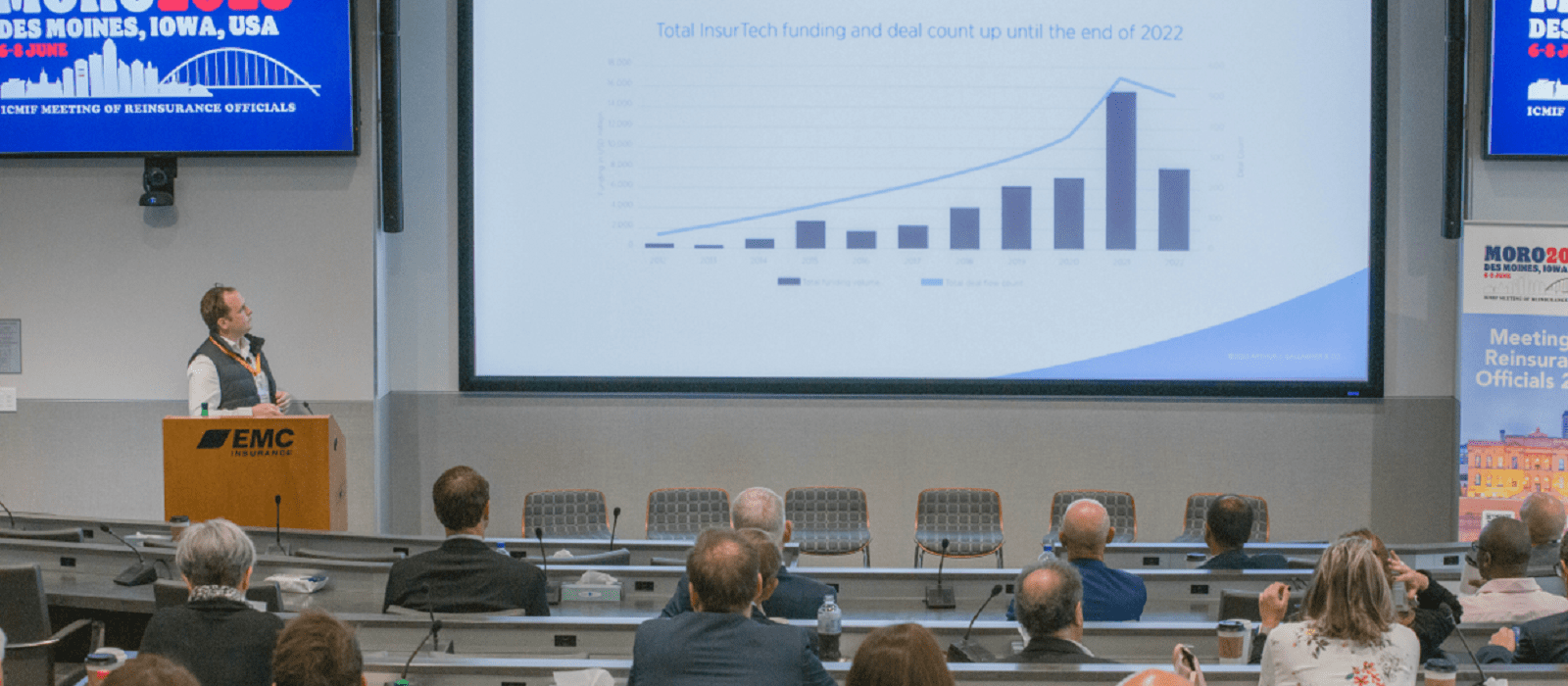

Investment in insurtech has experienced significant growth, with billions of dollars flowing into the industry. External investors, particularly technology venture capital firms from Silicon Valley, were attracted by the perceived growth opportunities and potential disruption within the insurance sector. However, the investment landscape has recently shifted. Funding has decreased due to macroeconomic factors and a realisation that the promised value from previous investments has not materialised as expected. Investors are becoming more discerning, seeking the expertise of insurance professionals before making further investments. While the investment numbers have declined, a few mega-round deals (above USD 100 million) continue to drive the headlines, highlighting the concentration of funding in a small number of companies.

Within the broad spectrum of insurtech, three key focus areas have emerged: distribution, business-to-business (B2B) support, and risk origination. Distribution is witnessing the rise of embedded insurance, which involves integrating insurance products seamlessly into other sales cycles. Affinity-based selling opportunities, where insurance products are offered at specific points of sale, are gaining attention. Insurtech is also proving valuable in supporting brokers and agents, disproving the initial notion that they would be replaced. B2B back-office support is another successful aspect of insurtech, with many companies leveraging technology to streamline their operations and improve efficiency.

Additionally, insurtech has played a significant role in risk origination. Using advanced data analytics, artificial intelligence, and machine learning algorithms, insurtech companies can assess risk more accurately and efficiently. This enables them to provide innovative insurance products tailored to specific customer needs and risk profiles. By leveraging technology, insurtech firms are enhancing underwriting capabilities, automating claims processes, and improving overall risk management.

While insurtech has shown great promise, it has also faced regulatory challenges. Insurance is a highly regulated industry, and the introduction of new technologies and business models has raised questions about compliance and consumer protection. Insurtech companies need to navigate complex regulatory frameworks to ensure they meet the necessary requirements.

To address these challenges, collaboration between insurtech startups and incumbent insurance players has become crucial. Established insurers and reinsurers bring their industry expertise and regulatory knowledge, while insurtech startups contribute innovative technology solutions. By collaborating, both parties can create synergies, improve customer experiences, and navigate regulatory landscapes more effectively.

For EMC, a 112-year-old mutual insurance company, digital transformation has been a significant driving force behind its ongoing innovation. Its digital transformation, encompassed changes in technology, people, business models, and processes to enhance interactions with digital assets. The primary goal of this transformation is to improve business processes, create new experiences, and provide exceptional customer service. While technology plays a crucial role, EMC acknowledges the importance of focusing on people, relationships, and challenging existing business models to achieve success.

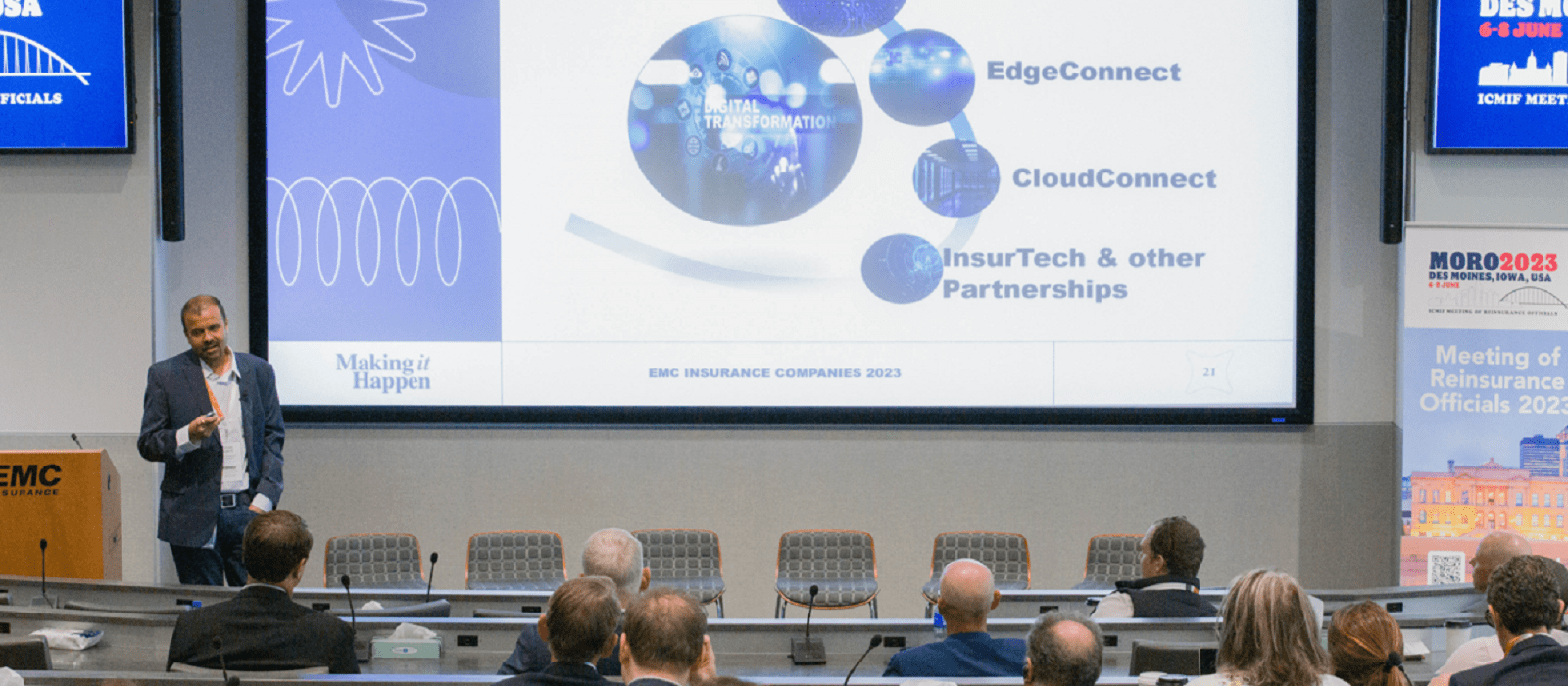

EMC’s technology transformation is categorised into three main programmes. The first programme, CoreConnect, aims to replace core platforms such as policy building, claims, and portals. EMC has adopted the Guidewire platform, leveraging its cloud-first instance advantage. The second programme, EdgeConnect, focuses on transforming non-core platforms and support systems, aiming to reduce the reliance on legacy systems such as Mapper and COBOL. Finally, the CloudConnect programme facilitates the migration of EMC’s data centres to the cloud, adopting a cloud-first approach and leveraging the capabilities of AWS.

The organisation attributes its successful transformation to three essential elements: insourcing strategy, data utilisation, and scale. The company capitalises on its deep insurance knowledge and invests in upskilling and reskilling its team members. While outsourcing partners are used strategically, EMC places a strong emphasis on developing in-house talent. The insurer has also implemented an enterprise data warehouse solution, empowering data-driven decision-making and streamlining transformation processes. Finally, EMC’s ability to scale its transformation efforts rapidly over the past three years has been instrumental in driving innovation and achieving significant milestones.

One of EMC’s insurtech partners is Betterview, a company that specialises in property intelligence and risk assessment for the insurance industry. It leverages advanced technologies such as computer vision, artificial intelligence (AI), and data analytics to convert disparate property data into actionable insights. Betterview’s platform ingests various property data sources, including aerial and satellite imagery, and processes them to extract valuable information about properties.

One of Betterview’s key offerings is their ability to analyse aerial imagery using computer vision and AI algorithms. By analysing the imagery, they can identify and assess different aspects of properties, such as the condition of roofs, materials used, and potential hazards. This allows insurance companies to make more accurate risk assessments and underwriting decisions. Betterview also provides proprietary risk scores and analytics based on the processed property data. These scores help insurers evaluate and price policies more effectively into their existing workflows.

EMC invested in Makusafe, a startup creating wearable tech for workers to track and improve employee safety using real-time data. The devices, known as “workforce wearables,” monitor four key areas: human motion, environmental conditions, worker voice, and data mapping. The Makusmart dashboard allows those in charge of safety to make immediate changes, prioritise tasks, improve worker safety, and boost productivity. Benefits reported back by organisations using the devices include increased morale as management respond to problems before workers have to file complaints, improvement in operational and economic efficiency, and safety improvements. Some workers raised concerns about data privacy, but, when addressed by leadership through being transparent about the data collected, it led to increased adoption.