The insurance sector is undergoing a significant transformation, moving beyond traditional risk transfer to embed resilience, prevention, and risk reduction into its core operational functions. This shift is particularly evident among mutual and cooperative insurers, who are leveraging their unique structures to deliver greater value to members and society at large.

Resilience is increasingly seen as a strategic imperative for insurers. By integrating prevention and risk reduction principles into claims, underwriting, and product development, insurers can reduce exposure, accelerate recovery, and strengthen their overall value proposition. This approach enables a transition from reactive models to forward-looking strategies, equipping insurers to manage and adapt to a landscape marked by rising and interconnected global risks.

The power of data-driven underwriting

A key driver of this transformation is the adoption of data-driven underwriting. Insurers are harnessing advanced analytics and nature-based solutions to better understand and mitigate risks. For example, studies have demonstrated that natural habitats, such as coastal protection, can significantly reduce insurance losses from catastrophic events. Despite this, such critical data is often absent from traditional underwriting files, highlighting the need for the industry to capture and utilise more relevant data to inform decision-making.

Claims management as a tool for building resilience

Claims management is another area where resilience can be operationalised. Rather than focusing solely on the speed of claims payments, insurers are encouraged to consider post-claim interventions that promote rebuilding with resilience in mind. This might involve incentivising policyholders to adopt stronger construction methods or advanced technologies, thereby reducing the likelihood and severity of future losses. Such an approach requires a willingness to invest in short-term costs for long-term gains, particularly when working with trusted partners such as mutual insurers.

Distribution and partnerships

Distribution channels, especially partnerships with banks, play a crucial role in scaling innovative insurance products. While bank distribution is not a new concept, its potential remains underutilised for delivering products that incorporate new data and claims practices. By leveraging established channels, insurers can increase penetration and ensure that resilience-focused products reach a broader audience.

Climate change, sustainability, and the insurance gap

The intersection of climate change and sustainability is reshaping the insurance landscape. Insurers are recognising the need to address both physical and transition risks associated with climate change. The sector is uniquely positioned to unlock climate financing, particularly in the renewable energy market, by providing the necessary risk transfer mechanisms that enable investment in sustainable projects.

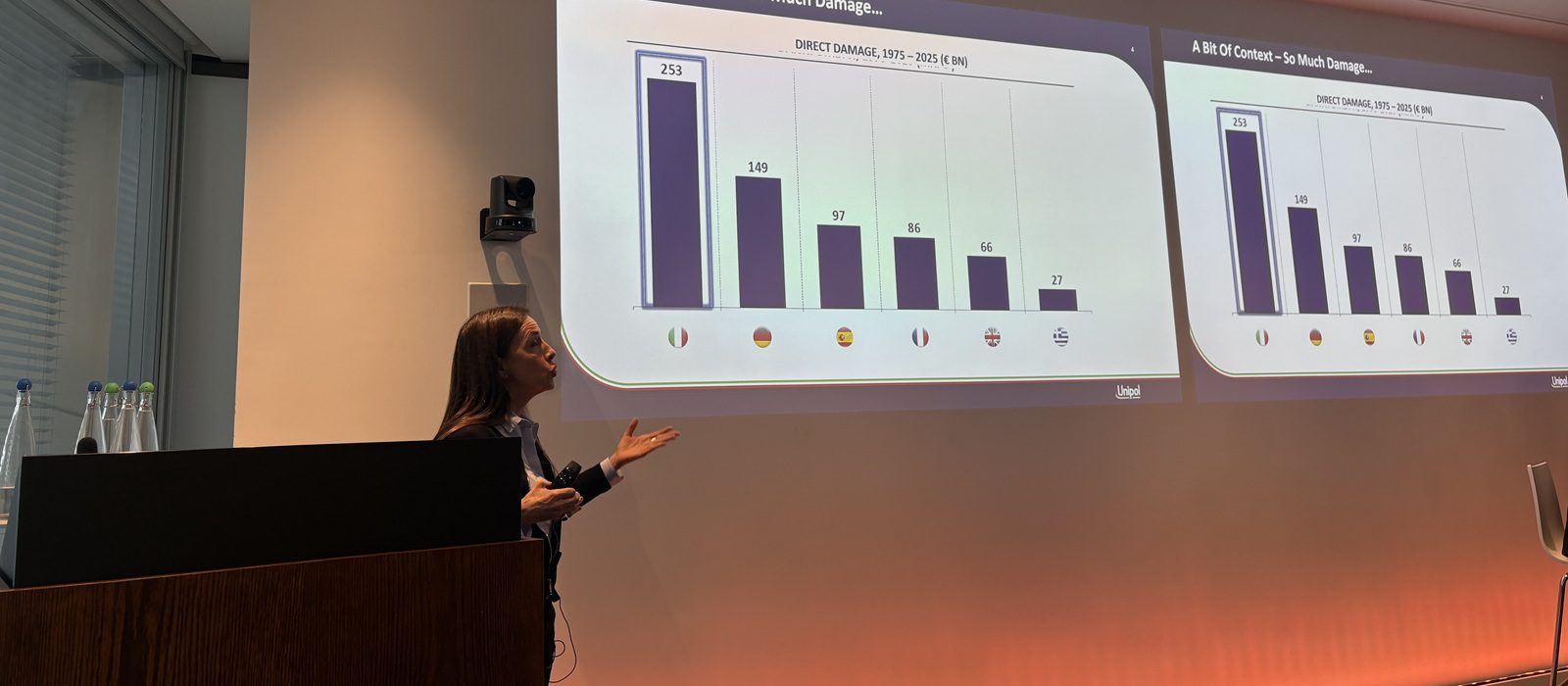

However, significant challenges remain. Many regions, such as Italy, face a substantial insurance protection gap, with a large proportion of homes and businesses lacking adequate coverage for catastrophic events. Addressing this gap requires not only regulatory interventions but also innovative product design, risk awareness campaigns, and digital platforms that facilitate access to insurance solutions.

The role of technology and partnerships

Technological innovation, particularly in data science and artificial intelligence, is enabling insurers to develop sophisticated models for assessing and pricing climate risks. Partnerships with scientific institutions and public administrations are essential for building tools that monitor and quantify extreme events, supporting both insurers and policyholders in making informed decisions.

Looking ahead: a call to action

The journey towards operationalising resilience is ongoing. Insurers are encouraged to share knowledge, foster dialogue, and build partnerships across the value chain. By focusing on practical measures that can be implemented today, such as improving data quality, embedding resilience in claims and underwriting, and leveraging distribution networks, the sector can make meaningful progress in reducing risk and enhancing societal resilience.

Ultimately, the integration of prevention and risk reduction across insurance functions is not only the right thing to do but also represents a compelling business opportunity. By supporting the transition to a more resilient and sustainable future, insurers can fulfil their vital role in society while ensuring their own long-term success.

Speakers:

- Nikhil da Victoria Lobo, Head of P&C Reinsurance for Western & Southern Europe and Middle East & Africa, Swiss Re (Switzerland)

- Zahra Jasmin-Uddin, Climate & Sustainability Analyst, Gallagher Re (United Kingdom)

- Giulia Balugani, Sustainability Manager, Gruppo Unipol (Italy)